Cementing Growth: The Strategic Evolution of North East India’s Cement Industry

The North Eastern Region (NER) of India—comprising Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, and Tripura—has long been known for its lush landscapes and cultural diversity. Yet, beyond its natural beauty, the region is undergoing a structural transformation powered by an unlikely driver: cement. This sector, historically peripheral to India’s industrial narrative, is now a central pillar in building the NER’s economic future.

Unlike other resource-driven stories, the cement industry in the North East is not merely about extraction. It is about integration—of resources, infrastructure, policy, and people. As government investment converges with private capacity expansion, the region is becoming a testbed for how industrial growth can reshape a frontier economy.

1. Market Landscape: A Small Footprint, Big Potential

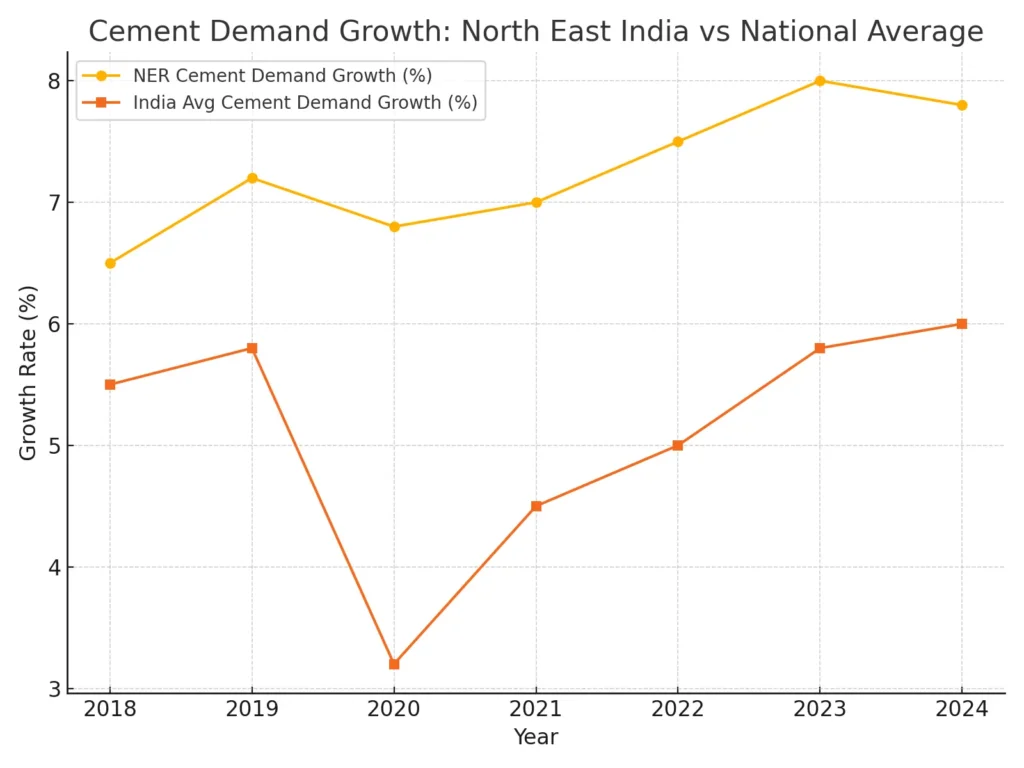

India is the world’s second-largest cement producer, with an installed capacity of 553 MTPA (April 2024). South India dominates with 32% of total capacity, while the East—including the North East—accounts for 20%. Within this, the NER is still a small contributor but one with disproportionately high growth potential.

- NER’s GDP share in India: 2.9%

- Assam’s GSDP growth (2022-23 to 2023-24): 19.1% vs. Maharashtra (10.93%) and Gujarat (10.09%)

- Per capita cement consumption (NER): ~131 kg/year vs. national average of 225 kg/year

- Demand growth: CAGR of 7–8% in recent years

The delta between current consumption and national benchmarks suggests a large headroom for growth. In essence, the NER is in a rapid catch-up phase, where cement consumption acts as a direct proxy for development.

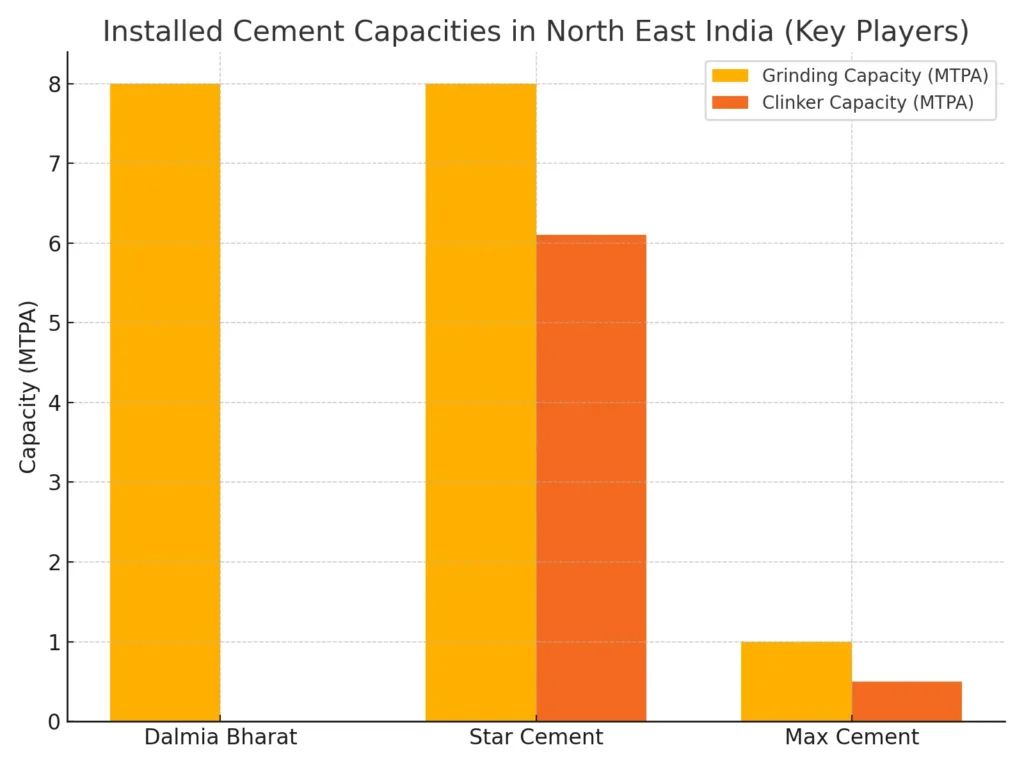

2. Supply-Side Dynamics: Capacity, Competition, and Clusters

The supply side of the NER cement market is marked by concentrated resources and aggressive competition. Meghalaya, endowed with ~9% of India’s limestone reserves, has emerged as the epicenter. Proximity to raw material gives producers a structural cost advantage.

Both Dalmia Bharat and Star Cement claim leadership. Dalmia emphasizes installed capacity and pan-India integration, while Star leverages entrenched regional presence and distribution. Expansion is intense:

- Dalmia Bharat: Plans new grinding capacity of 2–2.5 MTPA in the NER.

- Star Cement: Setting up two 2 MTPA grinding units in Silchar and Jorhat, investing ₹700–900 crore (FY2025–27).

This capacity race underscores the expectation of a sustained demand surge.

2.1 Other Regional and Public Sector Players

Besides the dominant private players, the NER’s cement ecosystem also includes mid-sized regional firms, a public-sector plant, and imports from Bhutan:

- Topcem Cement (Meghalaya/Assam): A grinding capacity of around 1.7 MTPA, focusing on the Assam and Meghalaya markets with a strong regional brand presence.

- Amrit Cement (Meghalaya): Established in 2012, Amrit operates an integrated plant in Jaintia Hills with 1.5 MTPA clinker capacity and 2 MTPA grinding capacity, serving both the NER and parts of Eastern India.

- Bokajan Cement Factory (CCI, Assam): Operated by the Cement Corporation of India, Bokajan is one of three functioning CCI plants nationwide. With an integrated capacity of ~0.2 MTPA, it is small but historically significant, offering steady employment in Assam.

- Bhutanese Supply: Plants in Bhutan—including Dungsam Cement Corporation Ltd (Dragon Cement) in Nganglam, Penden Cement Authority Ltd, and Lhaki Cement Authority Ltd in Gomtu—export cement into Assam, North Bengal, and other border markets. Dragon Cement, in particular, has sold a large share of its output in India since 2014.

While these players are smaller than Star and Dalmia, they remain relevant through niche positioning, local supply contracts, and cross-border trade, adding resilience and diversity to the North East’s cement market.

3. Demand-Side Drivers: Infrastructure and Housing

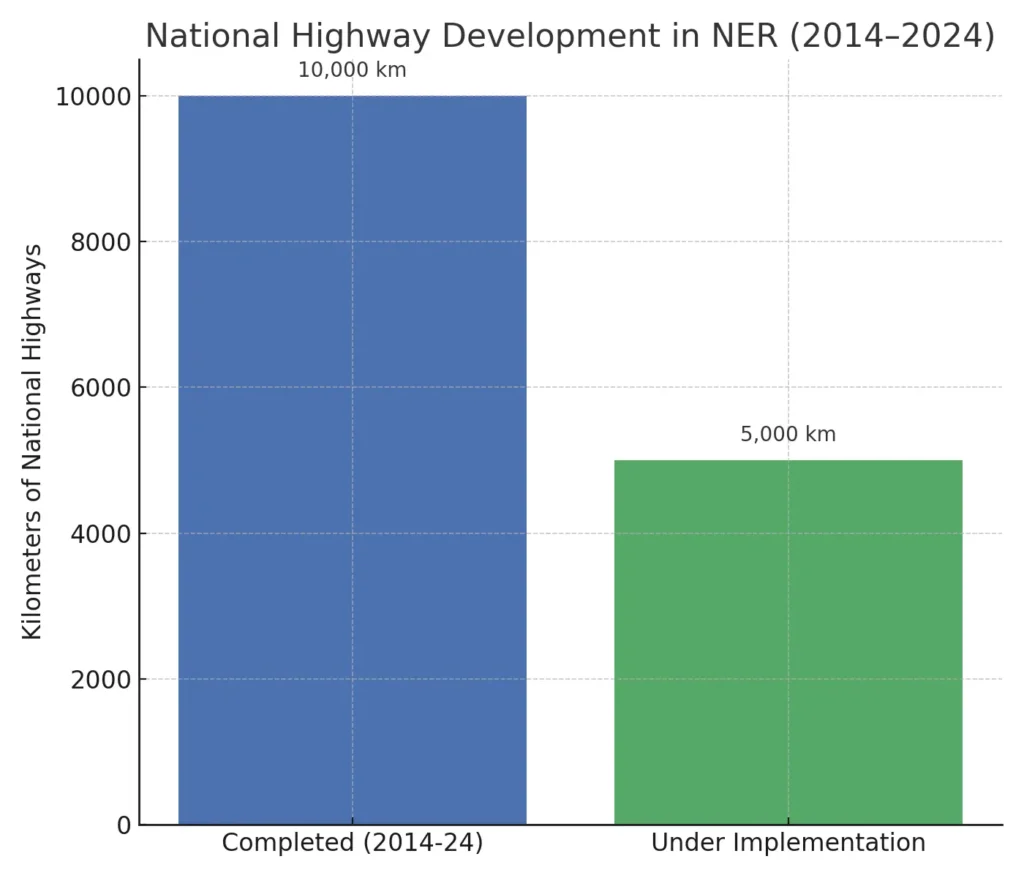

3.1 Infrastructure Pipeline

The government’s infrastructure push is the single biggest driver. Between 2014–2024, the NER saw the construction of nearly 10,000 km of National Highways at a cost of ₹1.07 lakh crore, with 5,000 km more under implementation.

Flagship projects include:

- Bogibeel Bridge: India’s longest rail-cum-road bridge across the Brahmaputra.

- Dhubri-Phulbari Bridge (under construction): Set to be India’s longest river bridge.

- Railway projects: Sivok-Rangpo (44.9 km), Bairabi-Sairang (51.3 km), and Jiribam-Imphal (110.6 km).

This is not cyclical spending but part of a multi-decade mandate under the Act East Policy and PM Gati Shakti, making infrastructure demand a stable floor for cement consumption.

3.2 Housing and Urbanization

While public infrastructure is the immediate demand engine, housing and commercial construction form the second growth wave. Nationally, housing consumes 55% of cement. In the NER, rising incomes and urbanization are translating into stronger residential demand, especially in Assam and Tripura. The combination of infrastructure + housing creates a dual-engine growth model, stabilizing demand beyond government cycles.

4. Logistics: From Bottleneck to Enabler

Historically, logistics has been the Achilles’ heel of the NER cement industry. Mountainous terrain, narrow roads, and landslides push freight costs to >40% of cement price. But this constraint is evolving.

- Rail Freight Growth (June 2025, NFR): 9.6% YoY increase in total freight, with cement freight up 53.1%.

- Emerging Multi-modal Solutions: Integration of rail, road, and inland waterways is lowering dependence on trucks.

This structural shift in logistics could fundamentally alter the cost curve, turning a historical disadvantage into a competitive advantage.

5. Environmental and Regulatory Landscape

The cement industry remains one of the 17 “highly polluting industries” under the Central Pollution Control Board (CPCB). Environmental risks in Meghalaya—deforestation, air pollution, and water degradation—are well documented.

- CPCB 2017 inspections: Found particulate matter emissions from some plants far exceeding norms.

- Community backlash: Reports of health impacts in plant-adjacent areas.

Compliance is therefore not optional—it is an existential factor. Companies investing in green cement technologies, efficient kilns, and ESG frameworks could gain a long-term competitive edge in a market where regulatory scrutiny will only intensify.

6. Economics: Profitability and Incentives

6.1 Company Performance

| Company | Period | Net Sales (₹ Cr) | Net Profit (₹ Cr) | EBITDA/Tonne (₹) |

| Star Cement | FY2025 | 2,893.7 | 220.7 | >1,500 (projected, medium-term) |

| Dalmia Bharat | FY2025 | 13,989 | 697 | 823 |

Despite national price volatility, the NER market has proven profitable for efficient operators. Star Cement, in particular, is projected to sustain high EBITDA margins, validating the region’s potential.

6.2 Government Incentives

The North East Industrial Development Scheme (NEIDS) offers:

- 30% capital investment incentive (up to ₹5 crore)

- 3% interest reimbursement on working capital

- GST & income tax reimbursement for 5 years

While implementation bottlenecks exist, these incentives de-risk capital-intensive projects, making the NER an attractive investment destination.

7. Challenges and Risks

- Logistics: Improvements are underway, but dependence on fragile terrain remains a long-term risk.

- Competition: With multiple players in expansion mode, margin pressure is likely.

- Environment: Compliance gaps can trigger regulatory penalties and reputational damage.

- Execution Risk: Delays in government projects could shift demand timelines.

8. Strategic Outlook

The NER cement industry is no longer peripheral. It is evolving into a high-growth, high-potential hub, underpinned by government policy, resource endowments, and private investment. But it is also a high-complexity market, where profitability hinges on three factors:

- Scale & Speed: Capacity additions must be timely to capture first-mover advantages.

- Logistics Mastery: Leveraging rail and multi-modal networks is crucial.

- Sustainability: A robust ESG strategy is no longer optional—it is a competitive differentiator.

From the limestone quarries of Meghalaya to the bridges across the Brahmaputra, the cement industry is quite literally laying the foundations of a new North East. The story is not without challenges—steep terrain, environmental scrutiny, and cutthroat competition. But with demand locked in through decades of public investment and rising private consumption, the industry’s trajectory points upward.

If stakeholders—government, corporates, and communities—can align growth with sustainability, the North East will not only build stronger infrastructure but also carve a stronger role in India’s economic future. The cement industry, once a background player, is now central to this transformation