The $2/kg Race: Can India Become the Global Green Hydrogen “Price-Maker”?

From the salt pans of Kutch to the docks of Paradip, a new energy map is being drawn.

For over a century, India has been a structural price-taker in global energy markets.

Oil prices were dictated by OPEC.

Gas contracts were indexed to volatile benchmarks.

Coal imports filled domestic gaps at global prices.

But green hydrogen presents a rare geopolitical inflection point.

As carbon border taxes tighten and industrial decarbonization accelerates, India is attempting something far more strategic than energy substitution — it is attempting cost leadership.

The $2/kg threshold is not just a number. It is a power shift.

The Global Context: From Climate Idealism to Industrial Physics

With the European Union’s Carbon Border Adjustment Mechanism (CBAM) moving into enforcement phases, exporters of steel, cement, fertilizers, and aluminum must now account for embedded carbon.

The message to emerging economies is blunt:

Decarbonize — or lose market access.

Under India’s National Green Hydrogen Mission, the country has committed to producing 5 million metric tonnes of green hydrogen annually by 2030, alongside massive renewable capacity expansion.

This is not climate symbolism. It is industrial defense.

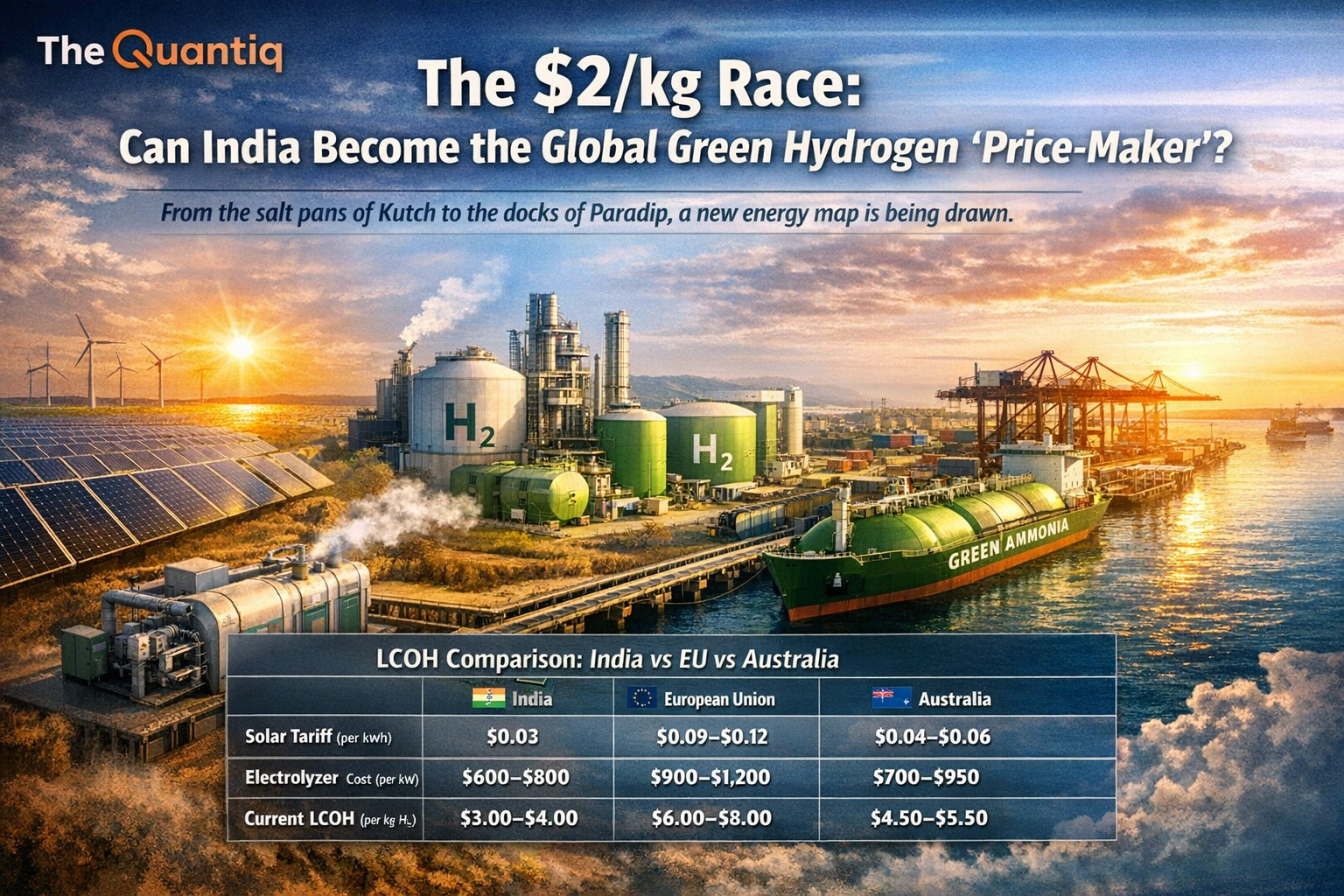

Cracking the LCOH Code: Verified Cost Comparison

The economics of green hydrogen are driven primarily by:

- Renewable electricity cost (60–70% of total cost)

- Electrolyzer capital expenditure

- Capacity utilization (load factor)

Below is a comparison using data from IRENA, IEA, and national auction benchmarks (2024–2025 ranges).

Green Hydrogen Cost Comparison (2024–2025 Estimates)

| Parameter | India | European Union | Australia |

|---|---|---|---|

| Utility-Scale Solar Tariff | ₹2.0–₹2.8/kWh (~$0.024–0.034) | $0.08–0.12/kWh | $0.04–0.06/kWh |

| Electrolyzer Capex | $600–900/kW | $900–1,200/kW | $700–1,000/kW |

| Current LCOH (Green) | $3.0–4.5/kg | $5.5–8.0/kg | $4.0–5.5/kg |

| Grey Hydrogen (Reference) | $1.5–2.5/kg* | $2.0–3.5/kg | $2.0–3.0/kg |

*Grey hydrogen varies depending on natural gas prices.

Sources: IRENA 2024 Hydrogen Report, IEA Hydrogen Review 2024, SECI Auction Data, EU Renewable Benchmark Data.

India’s structural advantage lies in ultra-low renewable tariffs combined with falling electrolyzer costs as domestic manufacturing scales.

If electrolyzer costs decline toward $300–400/kW by 2028 (a trajectory projected by multiple global agencies under scale conditions), India could realistically approach $2.5/kg before 2030.

Industrial Survival: Why Steel and Fertilizer Cannot Wait

Green hydrogen is not an energy transition luxury. It is a survival mechanism for export-heavy sectors. Hydrogen-based Direct Reduced Iron (H-DRI) is emerging as the only scalable pathway for low-carbon steel production. Without it, exporters face carbon penalties under CBAM-linked pricing frameworks.

Expected Hydrogen Purchase Obligations (HPO) — similar to Renewable Purchase Obligations — may mandate 10–15% green hydrogen blending in refineries and fertilizer plants. Such mandates:

- Create domestic offtake certainty

- De-risk capital investment

- Accelerate electrolyzer scaling

Industrial policy becomes demand architecture.

From Importer to Export Hub: The Green Ammonia Strategy

Hydrogen is difficult to transport. Ammonia (NH₃) offers logistical viability.

Ports such as:

- Kandla

- Tuticorin

- Paradip

are being evaluated as green ammonia export corridors.

India’s crude oil import bill has exceeded $150 billion in recent fiscal cycles. Even partial substitution through domestic green hydrogen integration represents structural macroeconomic relief.

Simultaneously, Japan, the EU, and South Korea are actively exploring long-term green ammonia procurement agreements.

If India captures a meaningful share of projected global ammonia trade by 2040, export revenues could rival segments of petrochemical trade.

This is not energy diversification. This is energy repositioning.

Risks and Structural Constraints

The pathway is promising — but not frictionless.

Key challenges include:

- Water availability in arid renewable zones

- Intermittency management and storage costs

- Transmission infrastructure bottlenecks

- Capital intensity

- Policy continuity risks

- Global competition (Australia, Saudi Arabia, Chile)

The race is competitive. The margins will be thin. The winners will be those who control input cost architecture.

The Sovereignty Question

Green hydrogen is not about replacing molecules.

It is about replacing dependency.

If India succeeds in:

- Maintaining ultra-low renewable tariffs

- Scaling domestic electrolyzer manufacturing

- Creating binding domestic demand

- Securing export corridors

Then it moves from price-taker to price-influencer.

The 20th century belonged to oil cartels.

The 21st may belong to cost-efficient electron economies.

The real question is no longer whether India can produce green hydrogen.

The question is whether India can control its price.https://thequantiq.com/the-carbon-economy-the-new-oil-of-the-21st-century/