The India–EU Mega Deal: How Much of the 25% Actually Lands in Northeast India?

On January 27, 2026, Narendra Modi stood beside Ursula von der Leyen at Hyderabad House in New Delhi and announced what both sides described, with little hesitation, as “the mother of all trade deals.”

It was a moment designed for scale. Nearly two billion people. A quarter of global GDP. A negotiation that had stretched across two decades finally finding closure.

For India, the announcement carried the weight of arrival.

For Northeast India, it demands a quieter, more precise question.

Not whether this is historic. But whether it is relevant.

A Deal of Scale, Not of Symmetry

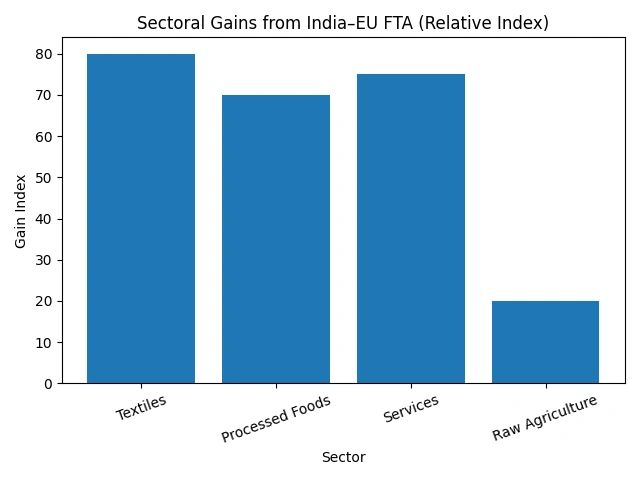

At the macro level, the India–EU Free Trade Agreement is difficult to overstate. The European Union is already India’s largest trading partner, with goods trade touching €120 billion in 2024 and services trade approaching €60 billion the year before. The agreement now pushes that relationship into a new phase, eliminating tariffs across the overwhelming majority of traded goods—over 90 percent on the European side, and close to that on India’s.

For sectors like textiles, leather, engineering goods, and handicrafts, tariffs that once hovered in the range of 10 to 17 percent are set to fall to zero. For services, the agreement opens doors across a vast spectrum—from IT to education to financial services—creating a more stable and predictable environment for Indian firms operating in Europe.

On paper, it is transformative.

But trade agreements, like all large structures, cast shadows. And in those shadows lie the details that matter most for regions like the Northeast.

The Line That Changes Everything

There is a sentence in the agreement—often relegated to footnotes in national commentary—that Northeast India cannot afford to overlook.

India has chosen to safeguard several “sensitive sectors.” Among them: tea, coffee, spices, dairy, poultry, cereals, and edible oils.

Read that again, slowly.

Tea.

Spices.

These are not peripheral commodities in the Northeast. They are the region’s economic signature, its export identity, its historical link to global markets. Assam’s orthodox tea, Lakadong turmeric from Meghalaya, ginger from Karbi Anglong, black rice from Manipur—these are not just products. They are narratives, deeply tied to geography, culture, and livelihood.

And yet, in the architecture of this deal, they sit largely outside the immediate gains.

This is not an omission. It is a design choice.

And it changes the equation entirely.

The Deal That Has Not Yet Been Signed

If the FTA is the headline, the real story for Northeast India lies in what is still under negotiation: the India–EU Geographical Indications agreement.

Because the Northeast is not poorly positioned in this trade story. It is differently positioned.

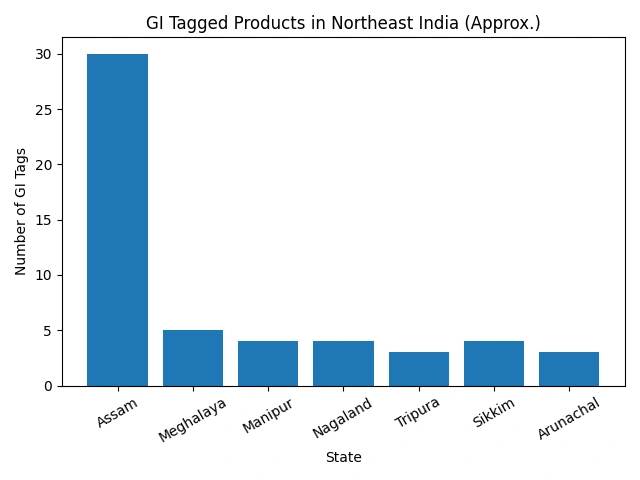

Across its eight states, the region holds one of the densest clusters of GI-tagged products in the country. These are not commodities competing on price. They are origin-certified goods competing on identity.

Muga silk from Assam, whose sheen deepens with time. Lakadong turmeric from Meghalaya, known for its unusually high curcumin content. Chak-Hao black rice from Manipur, rich in both colour and cultural memory. Naga King Chilli, Sikkim’s large cardamom, Tripura’s queen pineapple—the list reads less like a trade catalogue and more like a map of heritage.

European markets, particularly in countries like Germany and France, have spent decades building consumer cultures around precisely this kind of product—traceable, authentic, and rooted in place.

When the GI agreement is eventually concluded, these products will not simply enter European markets. They will enter with legal protection, with identity intact, and with the ability to command a premium that generic commodities cannot.

The difference between exporting turmeric and exporting Lakadong turmeric is not incremental.

It is categorical.

What Opens Now, Even Within Constraint

Despite the exclusion of bulk agricultural commodities, the FTA does not leave the Northeast untouched. It opens doors—but not always the ones the region is accustomed to walking through.

Textiles, for instance, quietly become one of the biggest beneficiaries. With tariffs dropping to zero, the Northeast’s handloom traditions—Muga and Eri silk, Bodo textiles, Moirang Phee, Naga shawls—suddenly find themselves aligned with European markets that value heritage, craftsmanship, and scarcity over scale. These are not products meant for mass retail. They belong in boutique stores, in curated collections, in spaces where story matters as much as fabric.

Elsewhere, the opportunity shifts from raw produce to processed value. The exclusion of tea and spices in their primary form does not extend to their derivatives. Ginger can travel as extract or oil. Turmeric can move as a high-curcumin nutraceutical. Black rice can become flour. Bamboo can enter as packaged food products. The logic is simple, but the implication is profound: value will accrue not at the farm gate, but at the point of processing.

And that is where the Northeast begins to encounter its own limitations.

The Invisible Opportunity: Services

There is another dimension of the agreement that has received far less attention, but may prove equally significant over time.

The FTA expands mobility across a wide range of service sectors, allowing Indian professionals to operate more seamlessly within the European Union. For the Northeast, this opens a pathway that is not tied to geography or logistics.

Cities like Guwahati are already seeing the early contours of a digital services ecosystem. At the same time, states like Meghalaya, Mizoram, and Manipur carry deep traditions of herbal medicine, natural wellness, and community-based healing practices.

Europe’s growing interest in integrative and alternative wellness systems creates an unexpected convergence.

Here, the Northeast does not compete on infrastructure.

It competes on knowledge.

Carbon, Compliance, and a Hidden Advantage

The European Union’s Carbon Border Adjustment Mechanism, or CBAM, is often viewed in India as a looming barrier. It imposes carbon-related costs on imports, effectively penalising high-emission production systems.

But in the Northeast, the story may be different.

Production here—whether agricultural or artisanal—is already low-carbon by default. Hydropower, biomass, and small-scale processes dominate. The challenge is not reducing emissions. It is measuring and certifying them.

If that infrastructure can be built, what appears today as a compliance burden could become tomorrow’s competitive edge.

The Constraint That Overrides Everything

And yet, all of these opportunities—textiles, processed goods, services, low-carbon exports—run into the same, persistent barrier.

Infrastructure.

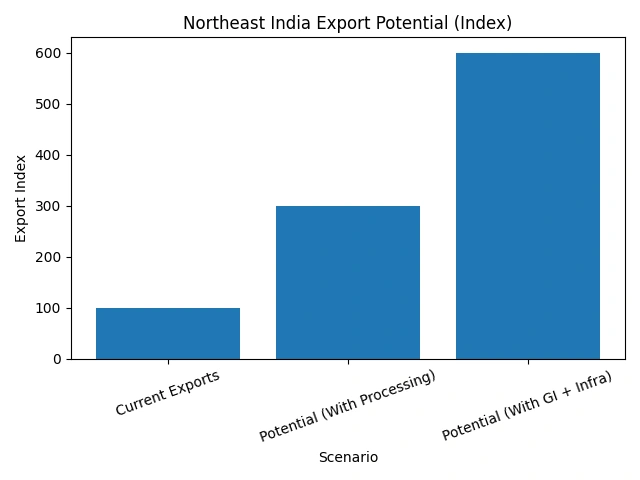

The Northeast’s export story is not constrained by lack of product. It is constrained by lack of systems. Cold chains remain fragmented. Processing units are limited. Logistics are expensive and often unreliable. Certification ecosystems are still in their infancy.

The numbers tell the story with uncomfortable clarity. Meghalaya’s exports, for instance, stand at just over ₹80 crore annually. For a region whose products can command premium pricing in global markets, this is not a reflection of demand. It is a reflection of capacity.

Trial shipments—Naga chilli to the UK, black rice to European markets—exist. But they remain exactly that: trials. The distance between a successful shipment and a sustainable export pipeline is measured not in kilometres, but in infrastructure.

The Time Between Now and Then

The FTA itself is not yet operational. It must pass through legislative processes in both India and the European Union. Legal vetting, translations, parliamentary approvals—all of this takes time.

Realistically, the agreement may come into force sometime between late 2026 and early 2027.

That window is not a delay.

It is an opportunity.

Because when tariffs fall, they will fall for everyone. The advantage will not go to those who notice first. It will go to those who are ready first.

The Quantiq’s View

The India–EU FTA is not a simple story of gain or loss for Northeast India. It is a layered, uneven, and deeply strategic shift.

The region’s traditional export strengths—tea and spices—find limited immediate advantage. But its deeper assets—GI-tagged products, artisanal textiles, low-carbon production systems, and emerging service capabilities—align remarkably well with the direction in which global markets are moving.

The opportunity, then, is not to export more of the same.

It is to export differently.

To move from raw commodity to value-added product.

From anonymity to identity.

From volume to premium.

The Final Question

The deal has been signed.

The door has been opened.

What remains uncertain is not the agreement itself, but the response.

Will Northeast India build the processing plants, the cold chains, the certification systems, and the logistics networks required to step through that door?

Or will it remain, as it has too often in the past,

a region rich in product, but poor in access?

Because in the end, the “mother of all deals” will not be judged by its scale.

It will be judged by who was ready when it arrived. https://thequantiq.com/beyond-the-resource-economy-the-capital-pivot-in-nagaland-tripura-manipur/