The IMF’s “Resilience” Paradox: Why India’s Growth Story Is Stronger Than Global Headwinds Suggest

At a time when much of the global economy remains trapped between inflation fatigue, geopolitical friction, and trade uncertainty, India continues to defy gravity. In its latest assessment, the International Monetary Fund has reaffirmed India’s position as the fastest-growing major economy, projecting growth well above most global peers for FY 2025–26.

Yet this optimism arrives amid rising external risks. Signals from Washington—under the new Donald Trump administration—suggest the possibility of fresh tariff pressures, including talk of incremental duties on imports from countries perceived to be bypassing sanctions through energy trade with Russia.

At first glance, the contradiction is stark:

How can India accelerate while the global system fragments?

The answer lies in what The Quantiq calls India’s “Resilience Paradox.”

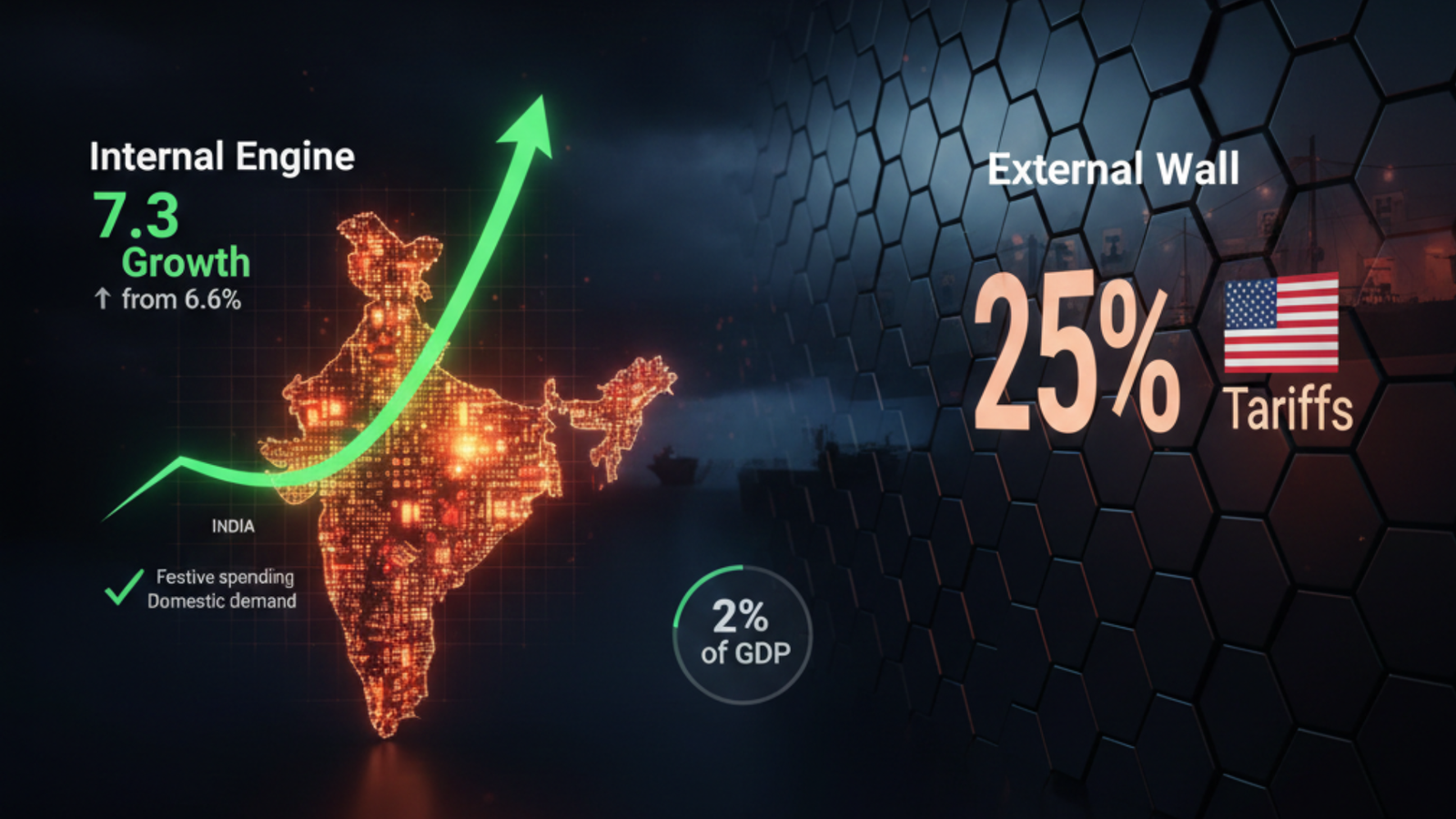

The Internal Engine vs the External Wall

India’s economy today is driven far more by internal momentum than by export dependence—a structural shift that many observers still underestimate.

🔹 The Internal Engine

- Robust festive and discretionary spending

- Rising urban consumption alongside rural recovery

- Large-scale public capex feeding private investment

- Digitisation driving efficiency across finance, retail, and logistics

Together, these factors have created a self-sustaining domestic demand cycle—one that cushions India against external shocks far better than in previous decades.

🔹 The External Wall

- Slowing global trade volumes

- Geopolitical fragmentation

- Potential tariff escalation by the United States

- Supply chain realignments driven by strategic mistrust

This wall is real—but its economic impact on India is often exaggerated.

The 2% Reality Check

Here’s the data point that reframes the entire debate:

India’s exports to the United States account for roughly 2% of GDP.

That makes US trade important—but not existential.

Even in a pessimistic scenario involving selective tariff hikes:

- The macroeconomic drag would be manageable

- The impact would be sector-specific, not economy-wide

- Domestic demand would continue to anchor growth

In other words, tariffs function less as an economic weapon and more as a geopolitical lever—designed to signal intent rather than derail growth.

Why the IMF Is Confident

The IMF’s sustained confidence in India rests on three structural pillars:

1️⃣ Demand-Led Stability

Unlike export-heavy Asian peers, India’s growth is consumption-driven, reducing exposure to global slowdowns.

2️⃣ Investment Cycle Revival

Public infrastructure spending has pulled private capex off the sidelines, particularly in manufacturing, logistics, and energy transition.

3️⃣ Institutional Digitisation

From tax collection to financial inclusion, India’s digital public infrastructure has compressed leakages and improved policy transmission—something global institutions now openly acknowledge.

These are not cyclical boosts. They are foundational shifts.

The Hidden Risk: Narrative Misreading

The real danger for India is not tariffs—it is misdiagnosing its own economy.

Excessive fixation on export threats can lead to:

- Defensive policymaking

- Overreaction to headline geopolitics

- Missed opportunities to deepen domestic reforms

India’s strategic task is not to insulate itself from the world, but to engage on its own terms, backed by internal strength.

A New Phase of Economic Confidence

India’s growth story no longer depends on global benevolence. It depends on:

- Sustaining domestic demand

- Deepening manufacturing competitiveness

- Reducing friction in capital and tax systems

- Staying geopolitically agile without economic panic

This is why the IMF sees resilience where others see risk.

The Quantiq View

Global headwinds make headlines.

Domestic engines drive outcomes.

India’s challenge is not surviving external pressure—it is recognising how far its economic centre of gravity has already shifted inward.

Growth, in today’s India, is less about what the world allows—and more about what the country enables.

One Comment